The Financial Sector Development Strategy looks to achieve economic growth through innovation, competitiveness, and facilitating greater access to banking

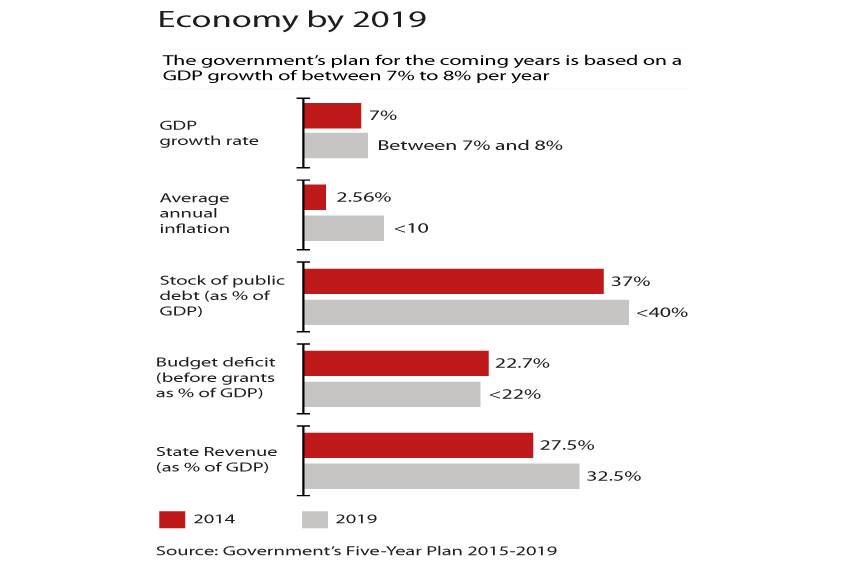

After Mozambique achieved independence in 1975, for many years the country’s socioeconomic development was based on a centrally planned, Marxist economy. The fact that Mozambique was surrounded by market oriented economies made it increasingly difficult for the country to develop. However, ever since the 1990s, when the government decided to open up its economy, with the International Monetary Fund (IMF) and World Bank imposing structural adjustment programmes that emphasised mass privatisation, trade liberalisation, currency devaluation, foreign investment, and stabilisation policies, Mozambique has been experiencing an unprecedented economic boom. Over the past decade, the country has grown at an average of 7 per cent a year – more than any country of the southern region of Africa – and has taken its place as one of the fastest developing nations in the world.

Ibraimo Ibraimo, CEO of Mozabanco, says the decision to change the country’s economic structure made the current rate of growth possible. “One of the first factors was the government’s political clarity to pass and create the market laws in Mozambique. There is much said about how Mozambique was a good pupil of IMF in some aspects. Today, there is a discipline to the economy’s structure as a whole…that’s why Mozambique is now one of the most institutionally functioning countries in Africa.”

Indeed today, Mozambique’s economy continues to grow strongly, largely thanks to prudent macroeconomic policy. The Financial Times magazine, The Banker, recently announced Ernesto Gove, the governor of Mozambique’s central bank, as ‘The Best Central Bank Governor in Africa 2015.’ According to the magazine, Gove’s efforts in Mozambique to contain inflation and increase international reserves have stimulated economic growth and stability.

As Mozambique persists with economic expansion, the development of the financial sector in particular is seen as key to the country’s future growth path. In 2013, the Mozambique Financial Sector Development Strategy 2013-22 was approved. At the base of the plan is achieving continued economic stability alongside three pillars of support: innovation; competitiveness; and facilitating greater access to the sector.

Increasing access

Today approximately 80 per cent of Mozambicans do not have access to formal financial institutions, and credit is only available to an estimated 3 per cent of the population. Such a dynamic means that Mozambique’s banking sector has some of the greatest potential for growth in Africa. However, Mr Ibraimo points out that such numbers may be misleading. “We have a banking index of 20 per cent, but the remaining 80 per cent is held by a nonmarket economy, so it is not bankable,” he says.

For this reason, even though there are 18 registered banks representing 95 per cent of total financial system assets, only three or four are present in rural areas; 85 per cent of the financial sector’s assets are concentrated in the three largest banks, all of which are foreign owned.

Total assets of the banking sector have recorded significant increases recently (up 19 per cent in 2013 compared to 2012, with profit after tax increasing by 32 per cent in the same year). KPMG’s report on the sector also highlights that returns on equity combined with efficiency levels indicate attractive returns.

Further significant growth in the sector, then, is possible, but it will only be attained by those bank institutions in Mozambique which have a mid to long-term project. “Mozabanco wants to do it…we want to transform into a universal retail bank, not only a bank that has presence nationwide,” says Mr Ibraimo. “The concept of universality we want to achieve is something that all the segments of the Mozambican society see in Mozabanco, their bank.”

This vision is related to the government’s plan of inclusion. Informal businesses count for 20-40 per cent of the country’s transactions. “These people cannot be ignored,” says Mr Ibraimo. He says that there are two ways to tackle this problem.

The first one is to reach out to these citizens with an organised and professional approach so they can be formalised. “They have to register with the government so they can have an account, then they must identify themselves, say where they live and what they do,” explains Mr Ibraimo. “Then we begin with financial literacy; they become aware of what a bank is and how to better manage their businesses.”

Another approach to the problem of inclusion is to build new satellite cities so that the country’s big centres become less crowded. This is something that will help in another aspect of the financial sector’s five year plan, which is the issue of economic diversification. People moving out of the city will likely be encouraged to work in agriculture, a sector Mozambique is seeking to develop further.

In order to get to access these people, Mozabanco is opening more branches, but the bank also wants to rely more on electronic banking. “The most important thing is that people can access the service,” says Mr Ibraimo.

Financing logistics

Another promising segment in banking is the demand coming from newly arrived companies to the country’s nascent oil and gas sector. Mr Ibraimo explains that there are two types of economy in Mozambique, the real one, that is, the one that encompasses sectors such as agriculture, fishing, and tourism, and the one that specialises in extracting natural resources like gas and coal.

“In the big exploration projects, when the multinationals arrive in Mozambique with their concession to explore these resources, they already have their logistics and financial projects closed,” says Mr Ibraimo. However, there are types of logistic services that can only be performed by local companies. “These companies are not ready; they do not have the capital to meet this demand. Mozabanco wants to support local small- and medium-sized enterprises (SMEs) so they are able to work as a bridge of logistic services for the great multinationals which will come in the process of exploration with big projects.”

Ecobank, the leading Pan-African bank which is present in 36 countries, is also looking to take advantage of the different opportunities available in Mozambique. “We are serving corporate customers, multinationals, regional companies, global companies, domestic and international organisations, among others. We are also operating in what we call the domestic banking segment, meaning, local corporate individuals, the public sector, and government companies,” says Adama Sene Cisse, Managing Director of Ecobank. “These two segments are supported by a platform of products, namely treasury and liquid management products. One can say we are offering a real range of products, be they designed for companies, entities or individuals.”

Cisse agrees with Ibraimo in terms of using technology to connect people in rural areas with banking: “We believe technology can bring people anywhere, we are trying to give our contribution towards financial inclusion by training, educating people, being innovative, and by bringing new products to rural areas.” She also says Ecobank is working to increase access to credits. The issues with credits, she says, are “due to, among other reasons, the lack of a customers’ database or of a credit bureau. We have to do more and better to serve our customers, and that includes facilitating the mechanisms through which they access credit.”

Facing the challenges

In face of such challenges, the government is preparing initiatives to improve the business environment. The approval of the regulatory framework for the creation of a credit bureau and the implementation of the EMAN II (Strategy for the Improvement of the Business Environment) should result in a more formalised economy as well as greater access to financing, easing the fiscal burden on SMEs, and enhancing SME productivity and competitiveness. However, the biggest constraint remains the lack of qualified human resources and general human development.

“The biggest challenge Mozambique faces in the agriculture sector is the lack of people educated to take advantage of the conditions that the land offers,” says Filipe Mandlate, KPMG’s Country Managing Partner. For Mandlate, an aspect that is able to foster faster agriculture improvement is the recently developed commercial agriculture, oriented to the domestic, regional, and international market. Additionally, growth is seen in the service sector – an area that is expected to increase even more with the developments brought by the discovery of gas.

“What we have been able to see is that Mozambique has the advantage of being a young and open country,” he says. Even though there is the language and corporate culture barrier – considering Mozambique is surrounded by English-speaking countries – he says that “the government is receptive and willing to make procedures easier to help the activities of the national and international private investor.”

0 COMMENTS